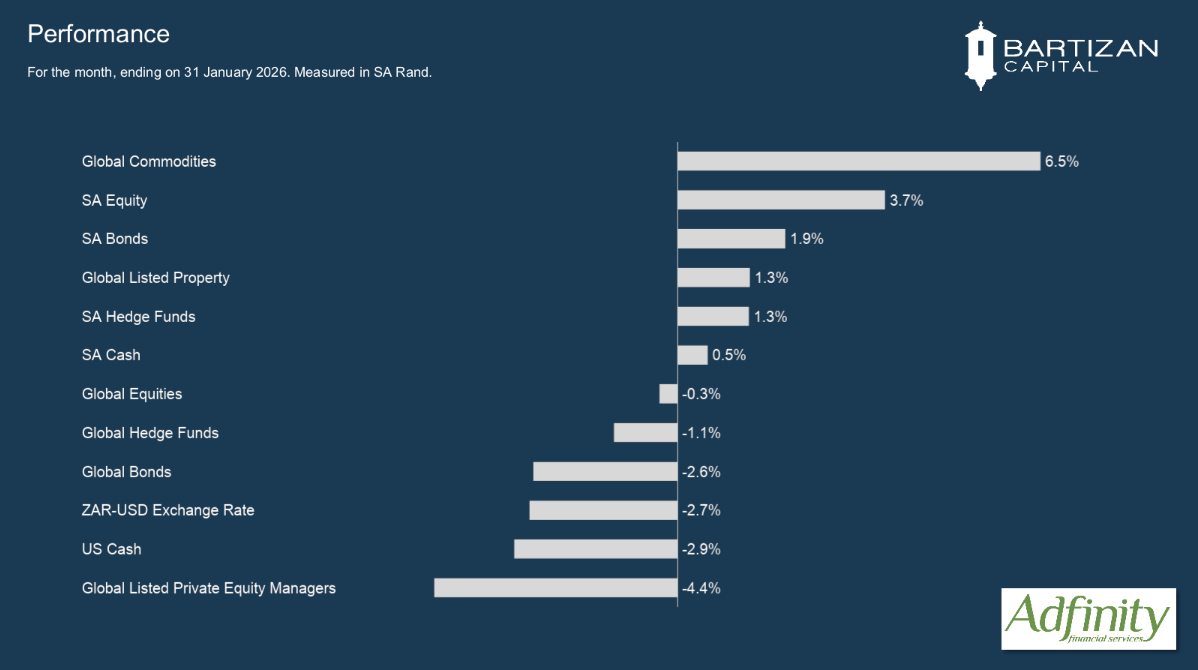

Market summary

A More Supportive Global Economic Backdrop

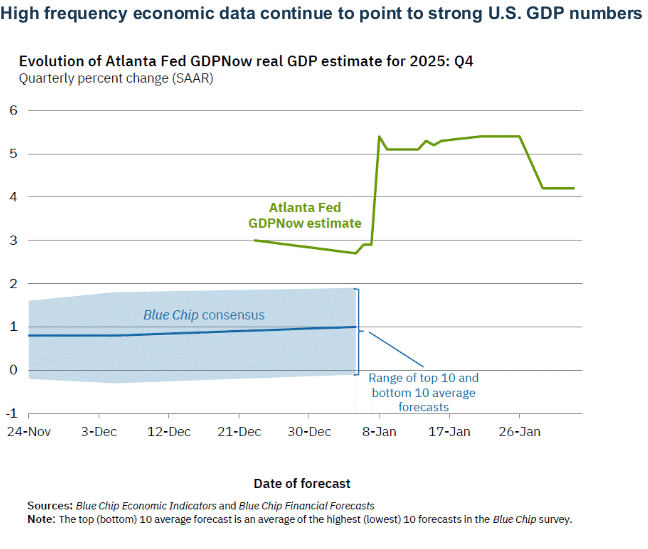

January was marked by eye-catching geopolitical headlines, but beneath the surface investor confidence improved. Economic data in the US and Europe surprised positively, while inflation continued to ease. This supportive mix of steady growth and cooling price pressures encouraged investors to take on more risk, helping global markets recover despite ongoing uncertainty.

Global Equities Benefit from Broader Market Leadership

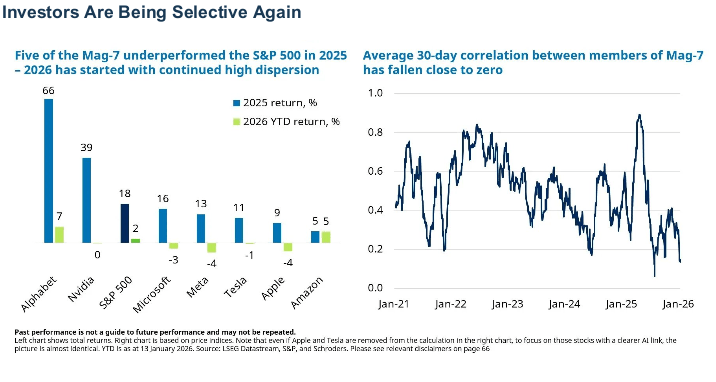

Global equity markets delivered solid gains as improving economic conditions broadened market participation. Performance was no longer driven by a small group of large US technology companies, with emerging markets, Japan and smaller companies outperforming. This shift highlighted the benefits of diversification, while defence-related stocks gained amid heightened global security concerns.

Bond Markets Adjust to Improving Growth Expectations

Bond markets faced some pressure as stronger economic data reduced expectations for early interest rate cuts. US and Japanese bond yields moved higher, reflecting policy and fiscal concerns, while European bonds were more mixed. Although bond prices struggled, higher yields improved long-term income prospects, reinforcing the role of bonds in balanced portfolios.

South African Markets Supported by Improving Fundamentals

South African markets had a positive month overall. Equities extended their strong run, led by mining shares, though late-month commodity volatility trimmed gains. Inflation continued to improve, allowing interest rates to remain unchanged, while government bonds performed well and the rand strengthened, reflecting growing confidence in the local economic outlook.

Markets Look Through Uncertainty

January proved volatile on the surface, with heightened geopolitical tensions making headlines, but investor confidence ultimately strengthened as the month progressed. Supported by better-than-expected economic data and easing inflation pressures, global equities rose around 3%, while government bonds struggled to gain traction as growth expectations improved.

Economic activity surprised positively across major regions. In the US and Europe, industrial production and manufacturing data exceeded expectations, while inflation prints were generally softer, pointing to improving real incomes. This “Goldilocks” backdrop encouraged investors to take on more risk, benefiting equities but weighing on bonds, particularly at the front end of the US curve and in Japan, where fiscal concerns pushed yields higher.

Broadening Returns Beyond US Mega-Caps

Global equity markets delivered solid gains in January, supported by improving economic conditions and stable inflation. Importantly, market performance became more evenly spread across regions and company sizes, rather than being dominated by a handful of large US technology stocks. Emerging markets, Japan and smaller companies outperformed, highlighting the value of diversification within equity portfolios. Heightened geopolitical risks also influenced sector performance, with defence-related stocks benefiting from increased focus on global security.

Correlation among the Magnificent Seven has fallen sharply, while return dispersion has increased. This points to a more selective market, where investors are rewarding strong fundamentals across a broader range of stocks rather than relying on a narrow group of market leaders.

Rising Yields Weigh on Government Bonds

Bond markets faced some pressure during the month as stronger economic data reduced expectations for early interest rate cuts. In the US, bond yields moved higher as investors adjusted their outlook for monetary policy, while Japanese government bonds experienced a sharp sell-off amid fiscal and political uncertainty. In Europe, bond performance was more mixed, with select markets benefiting from easing political risks and attractive income levels. While bonds struggled from a price perspective, higher yields continue to improve their long-term income potential.

Geopolitical Risk and Weather Drive Strong Gains in Commodities

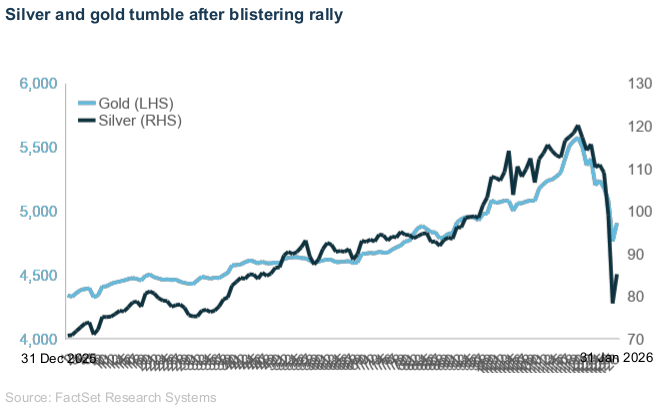

Commodities had a strong start to the year, providing valuable diversification benefits. Energy prices rose due to colder winter conditions and lower supply levels, while gold performed particularly well. Gold benefited from increased geopolitical uncertainty and ongoing demand from central banks, reinforcing its role as a defensive asset during periods of market stress. Gold and silver experienced a stunning “mania” as investors poured into precious metals amid geopolitical uncertainty and expectations of lower real yields, pushing prices to all-time highs – only for that parabolic rally to end abruptly: silver suffered one of the largest single-day percentage sell-offs on record, plunging over 30 % from its January peak in a matter of hours, underscoring just how extreme and volatile the speculative surge had become.

JSE Advances Further as Sector Performance Diverges

The South African equity market continued its strong start to the year in January, extending a rally that has now delivered substantial gains over the past two years. Performance was again led by mining shares, particularly gold and platinum producers, which benefited from higher commodity prices for most of the month. While the market made solid progress overall, a sharp fall in precious metal prices on the final trading day caused some late volatility and limited what could have been an even stronger monthly outcome.

Beyond the mining sector, performance was more mixed. Banks and selected financial companies delivered healthy gains, reflecting improving confidence in the local economic outlook and stable interest rates. In contrast, some large consumer and technology-linked shares came under pressure, despite generally sound business updates, as investors remained cautious about rising input costs and global political uncertainties. Overall, the JSE ended January higher, supported by strong commodity demand and improving sentiment, but with clear differences in performance across sectors.

South AfricA’s Inflation Progress Supports Bonds and the Rand

January was characterised by improving inflation dynamics and supportive bond market conditions in South Africa. The South African Reserve Bank kept interest rates unchanged at its January meeting, although the decision was more finely balanced than before, with two MPC members voting for a cut. Inflation data released ahead of the meeting showed further progress, with core inflation easing to 3.3% year-on-year, only marginally above the SARB’s newly emphasised 3% target. The rand strengthened during the month, briefly trading below R16 to the US dollar for the first time in nearly four years, before closing January at R16.15, benefiting from broad US dollar weakness.

Despite mixed global yield movements, South African government bonds performed well, with the 10-year yield falling to 8.05% – its lowest level in almost a decade – highlighting growing confidence in the domestic inflation outlook and providing a supportive backdrop for fixed income investors.

Disclaimer

The information and opinions contained in this document are recorded and expressed in good faith and in reliance on sources believed to be credible. No representation, warranty, undertaking or guarantee of whatever nature is given on the accuracy and/or completeness of such information or the correctness of such opinions. Bartizan Capital will have no liability of whatever nature and however arising in respect of any claim. damages. loss or expenses suffered directly or indirectly by the investor or the investor’s financial advisor acting on the information contained in this document. Furthermore. due to the fact that Bartizan Capital does not act as the investor’s financial advisor. they have not conducted a financial needs analysis and will rely on the needs analysis conducted by the investor’s financial advisor. Analytics recommend that investors and financial advisors take particular care to consider whether any information contained in this document is appropriate given the investor’s objectives. financial situation and particular needs in view of the fact that there may be limitations on the appropriateness of any advice provided. No guarantee of investment performance or capital protection should be inferred from any of the information contained in this document.

Bartizan Capital (Pty) Ltd is an authorised Financial Service Provider. FSP Number. 48450.