Market summary

Growth Broadens as Inflation Pressures Ease

February presented investors with a mix of geopolitical tension and encouraging economic data. The US Supreme Court ruled against using emergency powers to justify the April 2025 reciprocal tariffs, while tensions between the US and Iran escalated toward armed conflict late in the month.

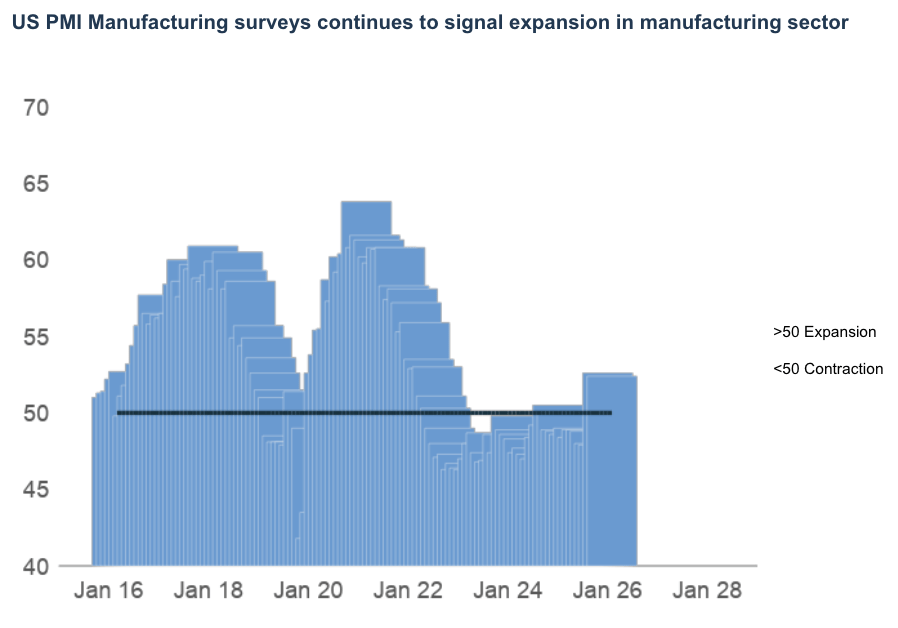

Despite this uncertainty, economic indicators remained constructive. Global business surveys signalled that growth continues to broaden across regions rather than relying on a handful of major economies. At the same time, inflation pressures showed further signs of easing in key markets including the US, UK and Japan, reinforcing expectations that central banks may have scope to ease policy later in the year.

In Europe, inflation surprised to the downside at 1.7% year-on-year, while UK inflation slowed to 3.0%, increasing the likelihood of near-term rate cuts. Overall, the combination of resilient growth and moderating inflation supported investor sentiment, even as geopolitical risks and structural shifts such as the long-term impact of artificial intelligence remain key considerations.

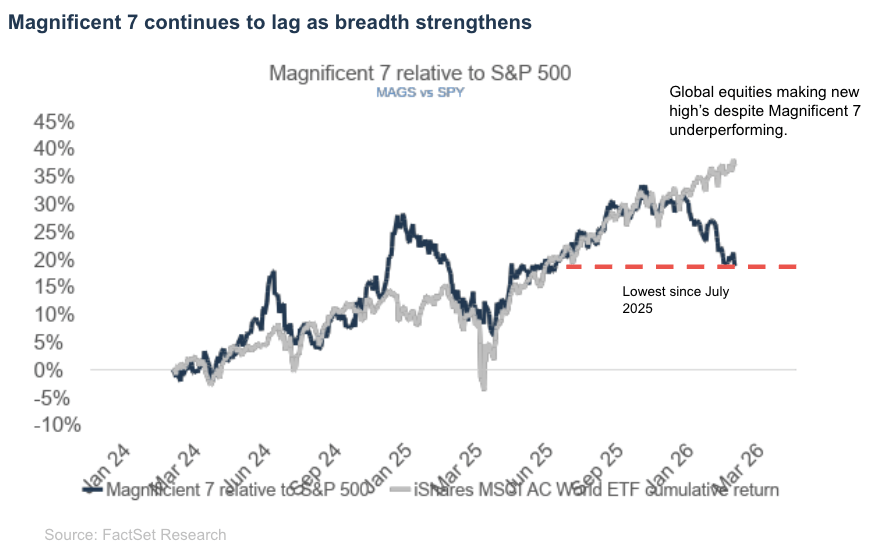

Rotation Away from Mega-Cap Tech Drives Market Leadership

Equity markets saw a notable shift in leadership during February as investors rotated away from mega-cap US technology companies. While the earnings season remained strong, markets increasingly questioned whether the massive capital investment required for artificial intelligence infrastructure will deliver sufficient returns.

This uncertainty weighed on US technology stocks and the S&P 500, which declined 0.8% over the month. Software companies were particularly affected as investors reassessed the durability of the “software-as-a-service” model in an AI-driven environment. Meanwhile, sectors linked to infrastructure and resource production outperformed. Materials, utilities and energy benefited from expectations that they will play a key role in the global build-out of AI infrastructure.

The rotation also supported value-oriented markets. Emerging market equities returned 5.5%, led by Asian manufacturers and Latin American commodity exporters. Japan was the standout performer, with the Topix rising 10.5% after Prime Minister Sanae Takaichi secured a decisive election victory, raising expectations for further fiscal stimulus.

Falling Yields Support Bond Returns

Fixed income markets delivered positive returns in February as investors sought the relative stability of high-quality assets. While economic growth remained resilient, rising geopolitical risks and concerns about the longer-term implications of artificial intelligence encouraged a move into bonds, pushing yields lower.

Global developed market government bonds returned 1.2% during the month. UK Gilts were the strongest performer, generating returns of 2.5% as inflation slowed to 3.0%, increasing expectations of near-term rate cuts from the Bank of England. Gilt yields declined by around 25 basis points over the month.

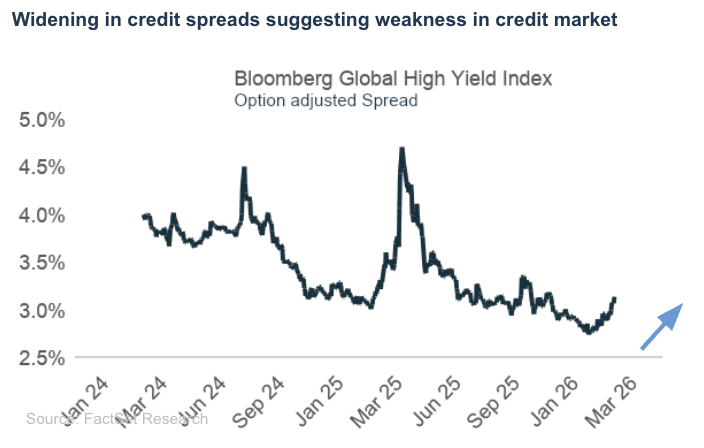

In Europe, weaker inflation and concerns about slowing demand also supported bond markets. Peripheral sovereign bonds, particularly those issued by Spain and Italy, outperformed German Bunds as higher starting yields boosted returns. Credit markets were more mixed. Investment-grade bonds returned 0.8% as spreads widened modestly, while emerging market local currency debt continued its strong performance, returning 1.4%.

Precious Metals Lead as Geopolitics Resurface

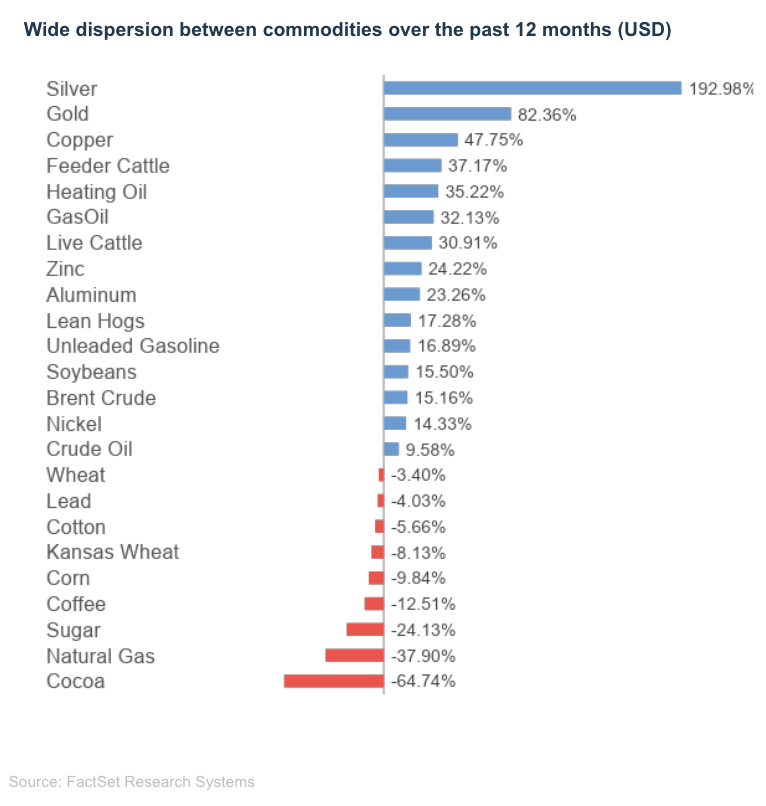

Commodities delivered modest gains in February, with the broader asset class returning 1.1%. Performance, however, varied significantly across sectors. Precious metals were the clear standout, rebounding strongly after a sharp correction in late January. Gold and related metals returned 12.4% during the month as falling bond yields and rising geopolitical tensions increased demand for safe-haven assets.

Energy markets were weaker for most of February as rising US inventories weighed on oil prices. However, this trend shifted sharply at the end of the month as tensions between the US and Iran escalated. The developments triggered a spike in oil prices when markets reopened in early March. Industrial commodities remained supported by signs of strengthening global manufacturing activity and expectations that the build-out of AI infrastructure will drive increased demand for key raw materials.

Local Markets Take the Spotlight

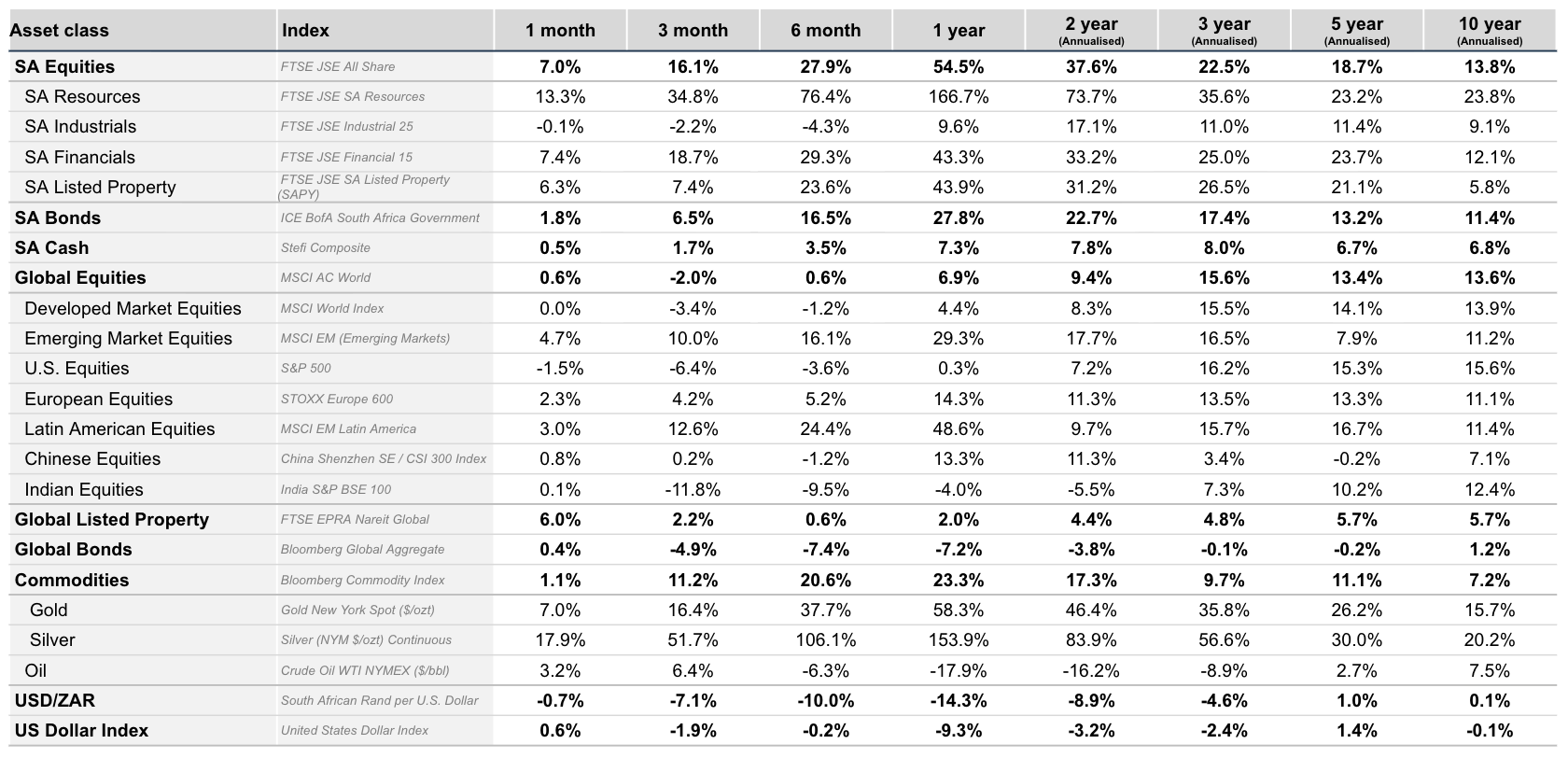

South African shares delivered another strong month in February, with the JSE rising about 7%, pushing year-to-date gains to roughly 11%. That places the local market among the better-performing markets globally so far this year. Over the past 12 months, returns look even stronger when measured in US dollars, helped not only by rising share prices but also by a firmer rand.

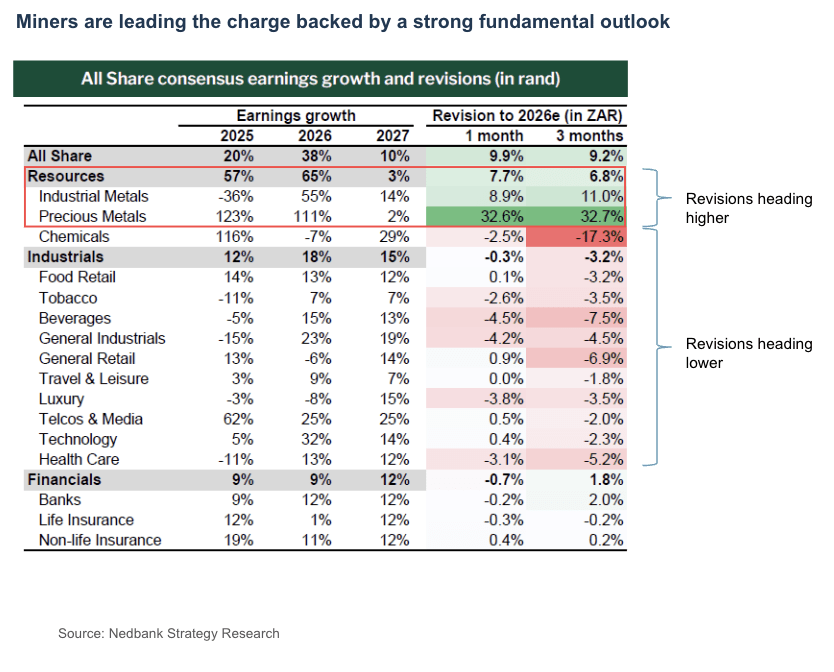

Mining companies, particularly gold and platinum producers, were a major driver of returns as commodity prices strengthened during the month. The gold price was volatile, dropping sharply early in February before recovering by month-end.

Companies linked to the domestic economy also performed well, with banks and insurers posting solid gains after encouraging updates from management. However, some large technology investment companies such as Naspers and Prosus weighed on the market, while retailers Pick n Pay and SPAR continued to struggle as their turnaround efforts remain slow to gain traction.

Steady Progress on the Economic Front

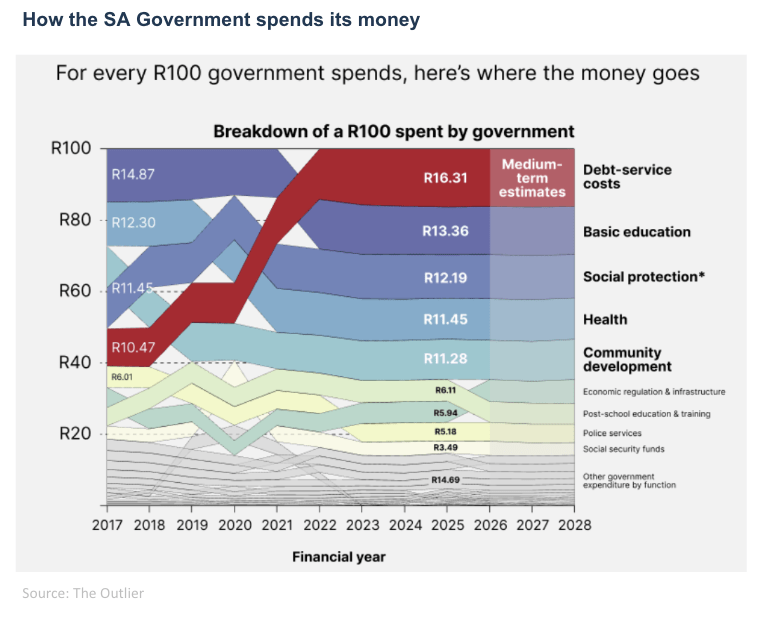

The broader economic backdrop also offered some positive signals. The latest South African Budget was generally well received by markets, with government continuing its plan to gradually improve the country’s finances.

Encouragingly, the budget points to a narrowing deficit and stabilising debt levels, helped by stronger revenue collection and higher commodity-related tax income. Importantly, this progress is expected without major tax increases.

At the same time, South Africa’s 10-year government borrowing rate remains close to 8%, near its lowest levels in the past decade. Lower borrowing costs help support confidence across financial markets and create a more stable environment for investments such as bonds and income-focused assets.

Major asset class performance (South African Rand)

Disclaimer

The information and opinions contained in this document are recorded and expressed in good faith and in reliance on sources believed to be credible. No representation, warranty, undertaking or guarantee of whatever nature is given on the accuracy and/or completeness of such information or the correctness of such opinions. Bartizan Capital will have no liability of whatever nature and however arising in respect of any claim. damages. loss or expenses suffered directly or indirectly by the investor or the investor’s financial advisor acting on the information contained in this document. Furthermore, due to the fact that Bartizan Capital does not act as the investor’s financial advisor, they have not conducted a financial needs analysis and will rely on the needs analysis conducted by the investor’s financial advisor. Analytics recommend that investors and financial advisors take particular care to consider whether any information contained in this document is appropriate given the investor’s objectives. financial situation and particular needs in view of the fact that there may be limitations on the appropriateness of any advice provided. No guarantee of investment performance or capital protection should be inferred from any of the information contained in this document.

Bartizan Capital (Pty) Ltd is an authorised Financial Service Provider. FSP Number. 48450.