Market Summary

Global Equity

Strong rebound during April as geopolitical risk eased

Global equity markets experienced a historic rebound in April 2026, largely shrugging off a severe geopolitical shock from the previous month to reach new all-time highs. The rally was defined by a powerful return to “risk-on” sentiment, primarily driven by a surge in artificial intelligence (AI) infrastructure investment, exceptionally strong corporate earnings and market sentiment improving following news of a potential ceasefire and resumed talks between the US and Iran.

The S&P 500 gained 10.4%, marking its best monthly performance since November 2020 and closing above the 7,200 threshold for the first time. The Nasdaq Composite surged 15.3%, driven by record-breaking performance in the semiconductor sector.

Emerging markets were the global standout, with the MSCI Emerging Markets Index reaching record highs. Gains were heavily concentrated in South Korea (+31%) and Taiwan, fueled by their critical role in the AI semiconductor supply chain.

European markets saw more modest gains, with the Euro Stoxx 50 rising 2.6%. Performance was constrained by Europe’s higher sensitivity to energy supply disruptions and a lack of heavy technology weightings compared to the US and Asia. Japanese equities gained 6.6%, participating in the global rally but hampered by record-high government bond yields and a more hawkish tone from the Bank of Japan

Global Fixed Income

Risk of higher inflation drives bond yields higher

Government bond markets were mixed in April, with performance largely driven by renewed inflation concerns following the rise in energy prices. Markets moved quickly to reprice the path of monetary policy, with expectations for rate cuts pushed out, or in some cases, replaced by further tightening.

Japanese government bonds (JGBs) were the worst performing over the month (-0.7%). While the Bank of Japan left interest rate policy unchanged, a more hawkish tone and upward revisions to its inflation forecasts led markets to bring forward expectations for further rate hikes. This change in market sentiment, combined with Japan’s sensitivity to imported energy, saw 10-year JGB yields rise to their highest level since 1997.

European government bonds were more mixed. Higher energy prices and weaker activity data pushed European yields higher at the beginning of the month, but a hold from the ECB saw German Bunds fall late in the month. UK Gilts also declined (-0.5%), reflecting a combination of inflation persistence and policy uncertainty.

By contrast, US Treasuries proved more resilient (-0.1%). As a net energy exporter, the US is less exposed to higher energy prices, while a more balanced growth backdrop helped limit the extent of the sell-off.

In credit markets, broader risk-on sentiment over the month saw spreads narrow, with performance largely reflecting differences in starting yields. Emerging market debt outperformed, supported by higher carry and a stable US dollar, followed by high yield and investment grade returns.

Commodities

The global supply of commodities remains uncertain due to the Middle East conflict

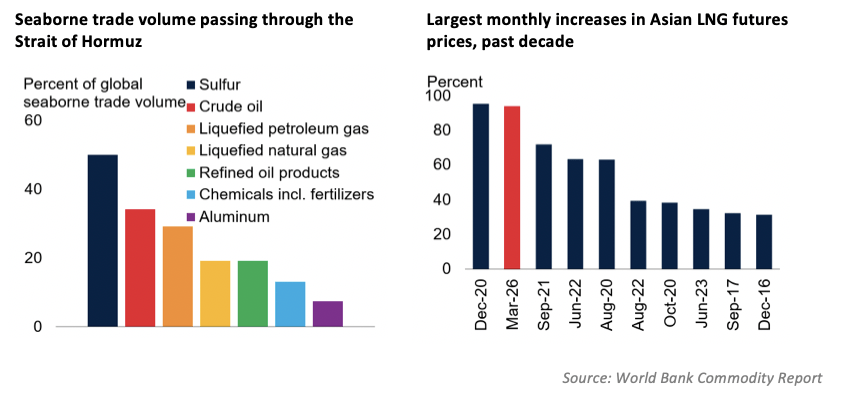

The Strait of Hormuz remained severely restricted during April, and oil pushed above $110 a barrel. The risks remain genuinely two-sided. A timely reopening of the Strait could see energy prices fall and rate expectations ease, while a continuation of the blockade could dampen activity and entrench inflation simultaneously.

Brent crude hit a four-year high of $126 per barrel during the month before easing toward $95/barrel as hopes for de-escalation emerged.

European and Asian natural gas benchmarks saw steep surges due to the reduction in Middle Eastern exports. US benchmarks (Henry Hub) remained more stable but still faced upward pressure as export facilities ran at near-peak capacity to meet global shortfalls.

Several key industrial metals reached all-time highs. Aluminium prices rose sharply due to both reduced exports from the Middle East and the soaring cost of energy used in its production. Despite the month-end decline, gold and silver experienced extreme volatility. Prices initially soared on safe-haven demand as the conflict began, but pulled back toward $4,650/oz later in the month following the start of US-Iran negotiations and profit-taking by investors.

Currencies

The dollar acts as a safe haven during risk-off

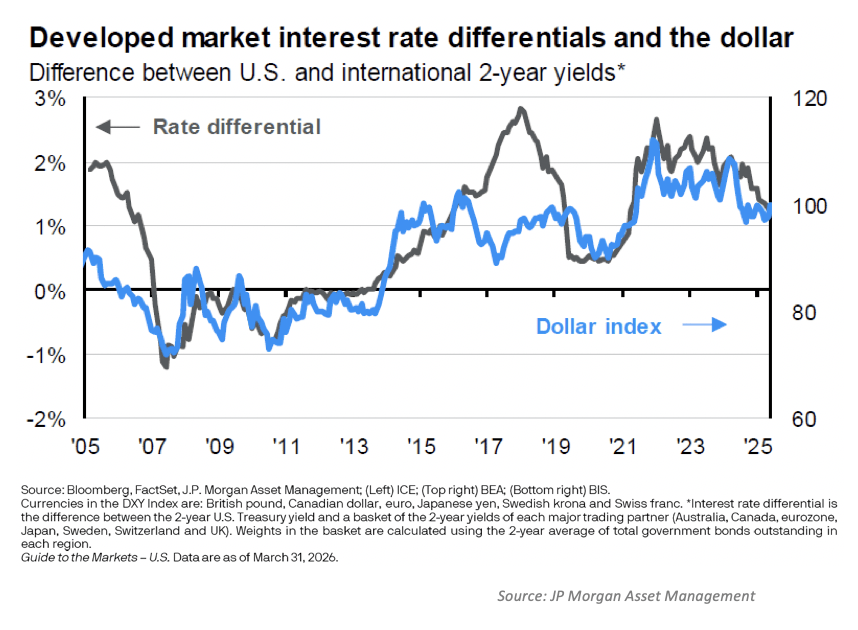

In April, currency markets were dominated by geopolitical volatility and shifting interest rate expectations. Last month, Dollar strength was driven by the effective closure of the Strait of Hormuz and a “hawkish hold” from the Federal Reserve. A potential de-escalation in the Middle East saw a decline in the Dollar Index during the first three weeks of April, but as risk-off sentiment started to build again towards the end of April, the Dollar Index started to recover. At the end of the month, the DXY was 1.9% lower.

Against the SA Rand, the Dollar traded at R17.20 at the start of the month, but as risk de-escalated, the Dollar reached a low of R16.16 on the 17th April, and then with risk returning to the market, the Dollar gained to close at R16.70 at the end of April.

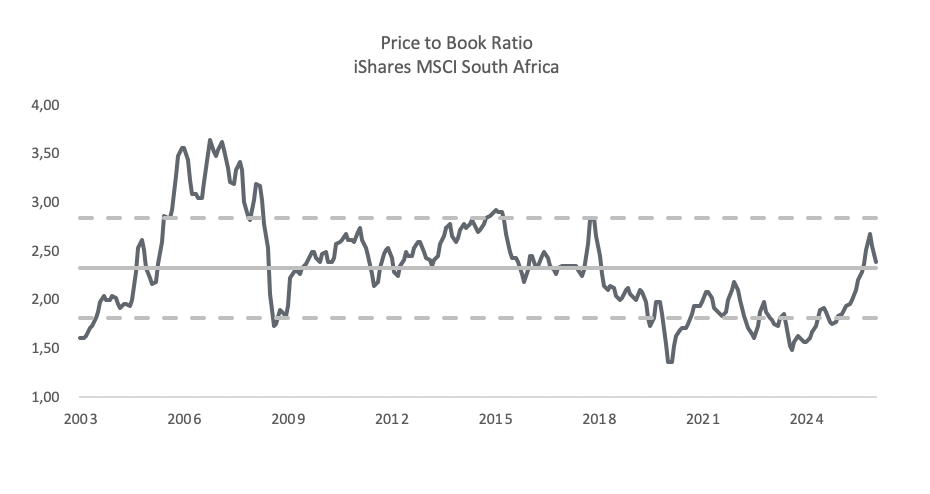

South African Equities

Broad recovery in share prices, but gold & platinum providers struggled

South African equities advanced 1.6% during April, supported mainly by local banks, consumer staples and healthcare companies.

The Financial Sector gained 4.3% for the month, with Investec Plc (9.6%), Investec Ltd (+8.7%), Standard Bank (+5.3%) and Capitec (+4.9%) all reporting strong gains. Life Insurance companies, Old Mutual and Sanlam, both declined in April.

Resources were pulled lower by declining gold and platinum producers. Despite strong gains from the diversified mining companies, Anglo American (+12.8%) and BHP Billiton (8.5%), the sector ended the month -2.6% lower.

The Industrial Sector delivered +3.0% for the month, with defensive sectors like consumer staples and healthcare outperforming the more cyclical sectors. Standout performance was recorded by Life Healthcare (+7.2%) and AB-Inbev (+6.6%).

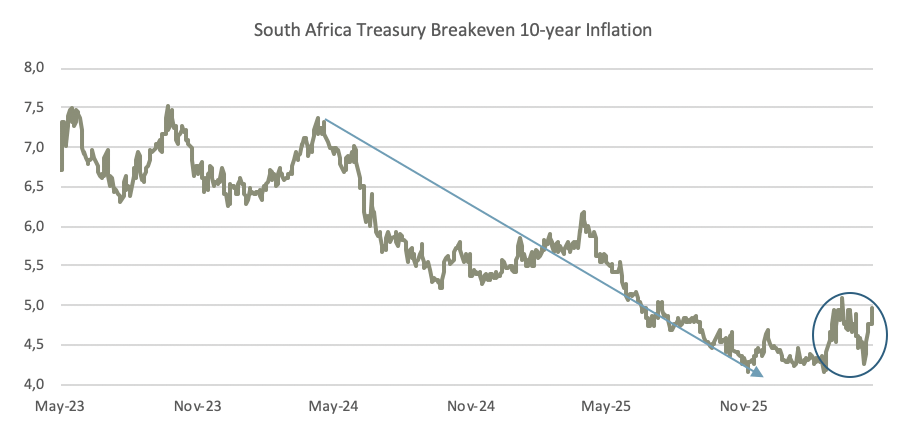

South African Fixed Income

Yields experienced a volatile month, as uncertainty about the Middle East caused the inflation premium to jump

A potential de-escalation of the conflict in the Middle East saw a decline in South African 10-year government bond yields, from 9.30% at the start of April to a low of 8.37% on the 17th of April. As confidence in the US-Iran ceasefire faded, 10-year bond yields moved back up, to end the month at 8.93%.

The major driver of the lower SA Bond 10-year yield over the past two years was the large decline in the inflation risk premium that is priced into the bond yield. The conflict in the Middle East and the uncertainty around energy prices have resulted in an increase in the volatility of the inflation premium, and since February, the premium has ranged between 4% and 5%.

The Satrix SA Bond ETF ended the month with a positive 4.2% return.

Disclaimer

The information and opinions contained in this document are recorded and expressed in good faith and in reliance on sources believed to be credible. No representation, warranty, undertaking or guarantee of whatever nature is given on the accuracy and/or completeness of such information or the correctness of such opinions. Bartizan Capital will have no liability of whatever nature and however arising in respect of any claim. damages. loss or expenses suffered directly or indirectly by the investor or the investor’s financial advisor acting on the information contained in this document. Furthermore, due to the fact that Bartizan Capital does not act as the investor’s financial advisor, they have not conducted a financial needs analysis and will rely on the needs analysis conducted by the investor’s financial advisor. Analytics recommend that investors and financial advisors take particular care to consider whether any information contained in this document is appropriate given the investor’s objectives. financial situation and particular needs in view of the fact that there may be limitations on the appropriateness of any advice provided. No guarantee of investment performance or capital protection should be inferred from any of the information contained in this document.

Bartizan Capital (Pty) Ltd is an authorised Financial Service Provider. FSP Number. 48450.