Market Summary

Volatility Returns as Geopolitics and Policy Uncertainty Rise

The first quarter of 2026 has been marked by heightened volatility, as markets navigated a complex mix of geopolitical tensions, policy shifts and evolving investor sentiment. While economic fundamentals remained relatively stable, external shocks – most notably the escalation of conflict in the Middle East -significantly altered the investment landscape.

At the same time, policy uncertainty resurfaced following developments around US trade tariffs, adding another layer of complexity. Markets increasingly focused on inflation risks rather than growth concerns, particularly as energy prices surged. This shift led to a broad-based sell-off across both equities and bonds, while previously popular trades – such as gold and emerging market equities -unwound. The US dollar strengthened as investors sought safety.

Market Leadership Broadens Beyond Big Tech

Equity market performance was mixed, with a clear rotation away from growth-oriented sectors toward value. Mega-cap US technology stocks came under pressure as investors questioned the sustainability of returns from rising artificial intelligence-related capital expenditure. This saw growth stocks decline meaningfully, while value stocks delivered modest gains.

Regionally, emerging markets proved relatively resilient despite late-quarter weakness, while Japan stood out as a top performer. The TOPIX Index benefited from a weaker yen and supportive domestic policy expectations following political developments. In contrast, US and European equities declined, weighed down by geopolitical risks and higher input costs. The UK market was a notable exception, supported by its exposure to commodity-linked sectors and currency tailwinds.

Bonds Under Pressure as Inflation Concerns Reprice

Fixed income markets experienced a challenging quarter as rising energy prices reignited inflation concerns. Government bonds sold off globally, with short-dated yields moving higher as markets shifted from expecting rate cuts to pricing in potential rate hikes.

While US Treasuries proved relatively resilient, supported by the country’s status as a net energy exporter, European and UK bonds faced greater pressure given their higher exposure to energy price shocks. Central banks responded with a more cautious tone, increasingly highlighting upside inflation risks and signalling a willingness to act if needed.

Credit markets weakened over the quarter, with spreads widening across both investment-grade and high-yield bonds. Emerging market debt also came under pressure, reflecting a stronger US dollar and increased global risk aversion.

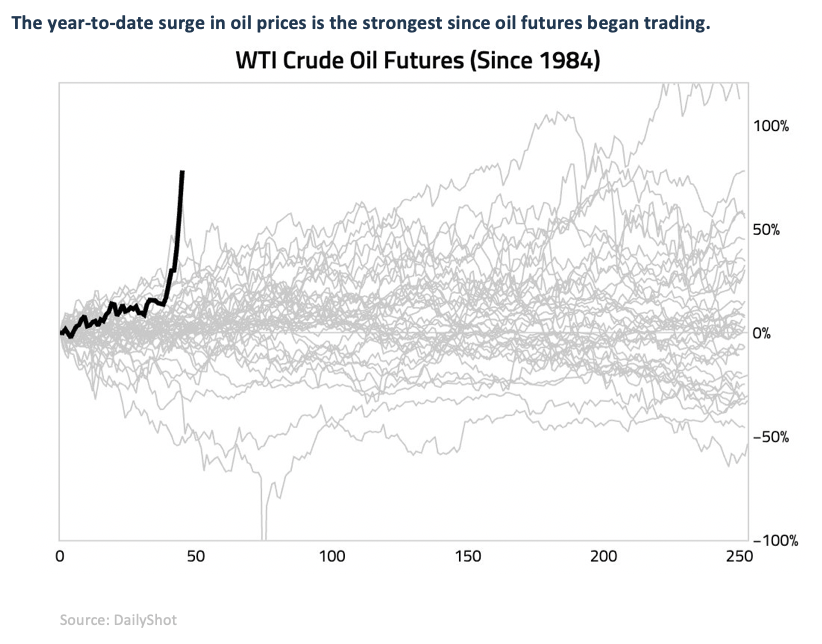

Energy Shock Drives Commodity Surge

Commodities were the standout performers during the quarter, with the Bloomberg Commodity Index rising an impressive 24.4%. The primary driver was a sharp increase in oil and gas prices following disruptions to Middle Eastern energy supply, including the effective closure of the Strait of Hormuz – a critical global trade route.

Brent crude oil surged by 63% in March alone, marking its largest monthly increase in decades. Beyond energy, agricultural commodities also moved higher, reflecting the importance of the region for global food supply chains. This broad-based commodity strength highlights the growing sensitivity of markets to geopolitical developments.

Markets Hit Pause After a Strong Run

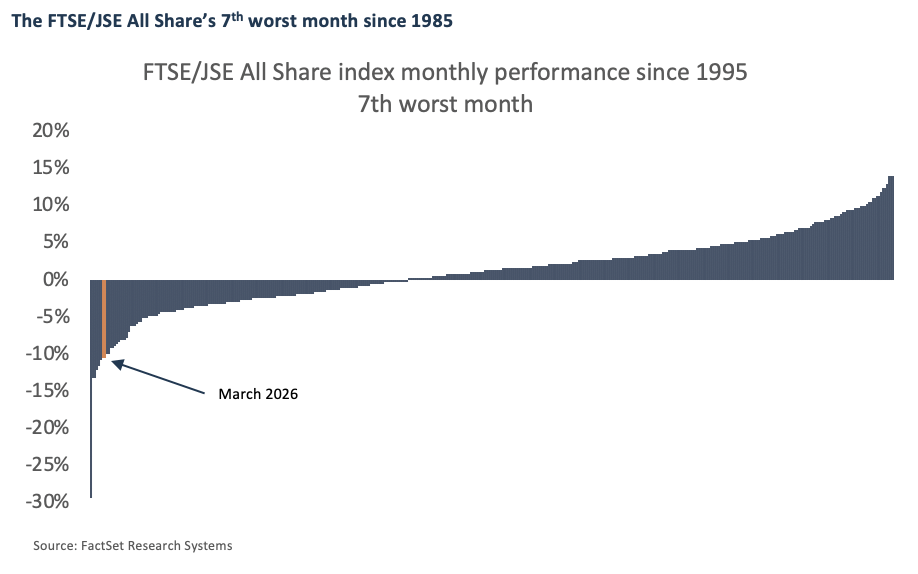

March proved to be a tough month for South African markets, bringing an abrupt end to what had been a strong run for local equities. The FTSE/JSE Capped All Share Index fell by 10.5% over the month, with a late 1.6% rebound on the final trading day helping to avoid what could have been the worst monthly decline since the global financial crisis. A large part of the weakness came from the precious metals sector, which had previously been a major driver of performance. Gold and platinum miners were hit particularly hard, declining by 18% and 25% respectively. This mirrored sharp drops in the underlying commodity prices – gold fell 12% during the month (at one point down nearly 25% before recovering), while platinum declined 18%, giving back some of its recent strong gains.

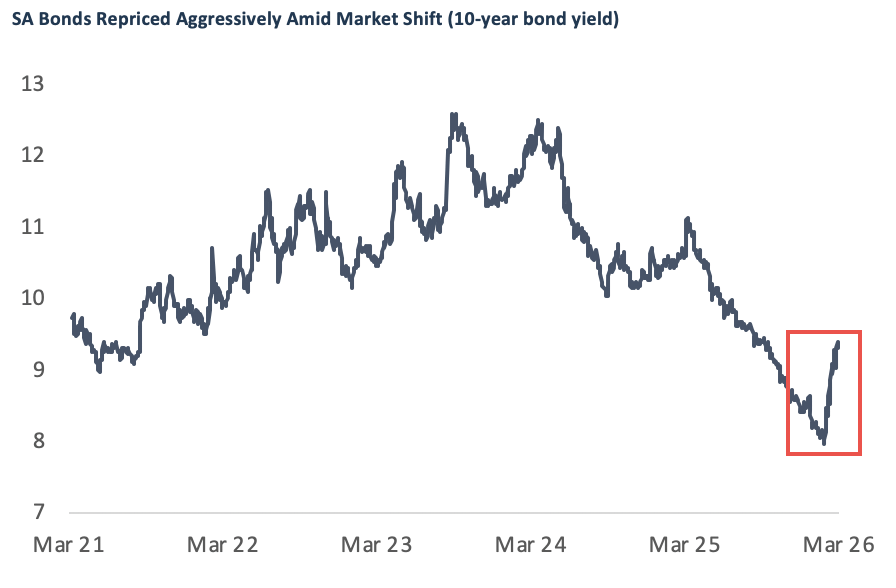

The pressure extended beyond equities. The local bond market also experienced a significant sell-off, with the All Bond Index falling 7% – its second-worst month in 25 years. This was driven by a sharp increase in government borrowing costs, with the 10-year bond yield rising to 9.3%.

Rates on Hold Amid Rising Uncertainty

On the policy front, the South African Reserve Bank kept interest rates unchanged at 6.75% at its March meeting, in line with expectations. This decision came shortly after inflation data showed prices increasing in line with the SARB’s revised 3% target. However, this data did not yet fully reflect the recent spike in energy prices, which remains a key area of uncertainty going forward.

The rand also had a challenging month, weakening by 5.9% against a stronger US dollar as global investors sought safer assets. While this erased the currency’s gains for the start of the year, it’s worth noting that the rand is still meaningfully stronger compared to a year ago.

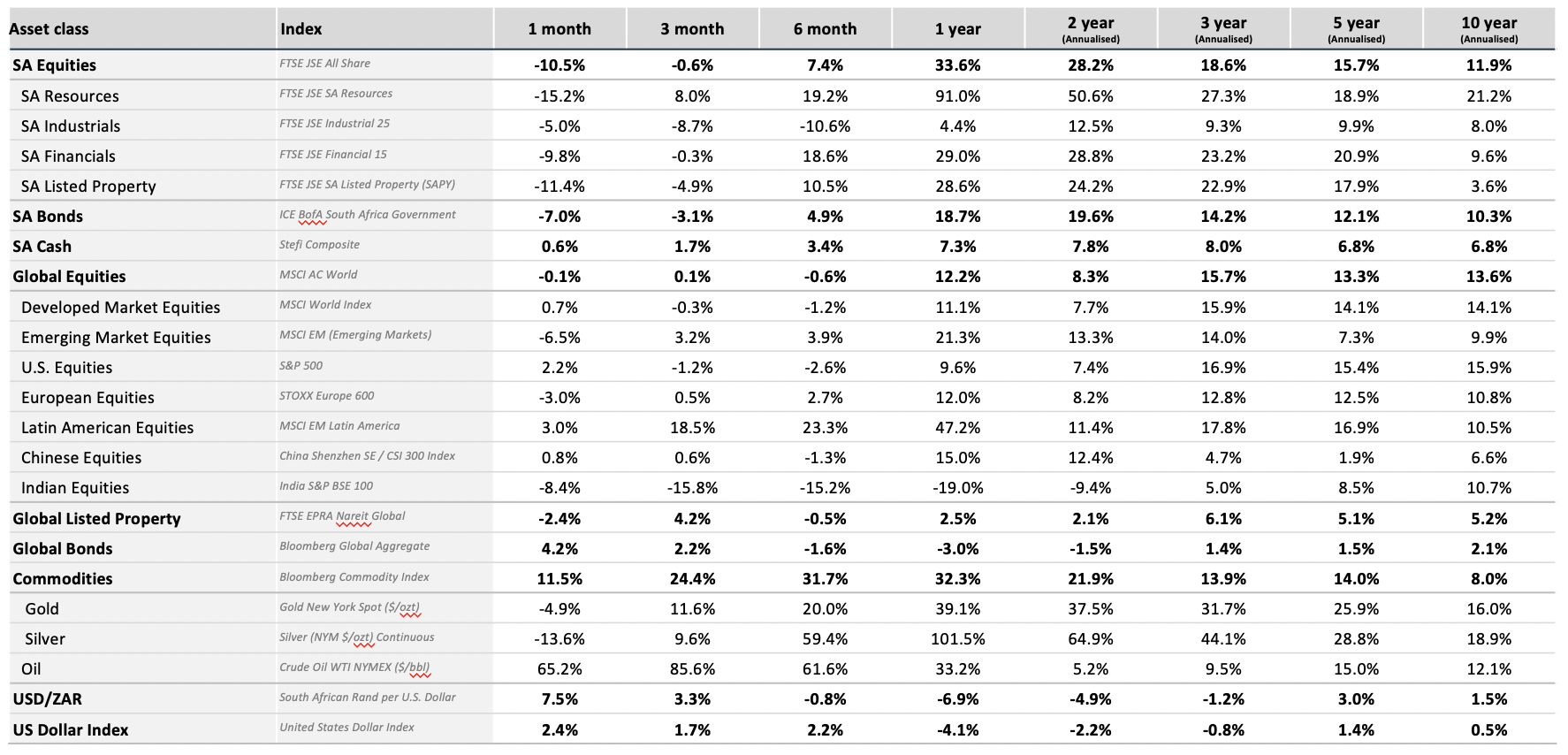

Major asset class performance (South African Rand)

Disclaimer

The information and opinions contained in this document are recorded and expressed in good faith and in reliance on sources believed to be credible. No representation, warranty, undertaking or guarantee of whatever nature is given on the accuracy and/or completeness of such information or the correctness of such opinions. Bartizan Capital will have no liability of whatever nature and however arising in respect of any claim. damages. loss or expenses suffered directly or indirectly by the investor or the investor’s financial advisor acting on the information contained in this document. Furthermore, due to the fact that Bartizan Capital does not act as the investor’s financial advisor, they have not conducted a financial needs analysis and will rely on the needs analysis conducted by the investor’s financial advisor. Analytics recommend that investors and financial advisors take particular care to consider whether any information contained in this document is appropriate given the investor’s objectives. financial situation and particular needs in view of the fact that there may be limitations on the appropriateness of any advice provided. No guarantee of investment performance or capital protection should be inferred from any of the information contained in this document.

Bartizan Capital (Pty) Ltd is an authorised Financial Service Provider. FSP Number. 48450.